Understanding Equifax Credit Score: Your Ticket to Smarter Car Loan Decisions

A practical guide to Equifax credit scores in Canada - learn how they work, why they matter for car loans, and how to use them to your advantage.

Summarize this blog post with:

Every time we help someone apply for a car loan, we end up talking about credit scores. Especially the Equifax credit score. Most folks know it matters, but few really understand how it shapes their financial future - or why lenders care so much.

Watching someone’s face change when they realize how their score impacts loan approvals, rates, and options is something we see every day. The truth is, knowing your Equifax credit score isn’t just about numbers. It’s about giving yourself the best shot at the car you want, on terms you can live with.

Key Takeaways

- Your Equifax credit score in Canada ranges from 300 to 900 and directly affects your car loan eligibility and interest rates. [1]

- Payment history, debt levels, and credit age are the biggest factors influencing your score - and you can control them.

- Regular score checks and simple credit habits go a long way, especially before applying for a car loan through us or any Canadian lender.

Understanding Equifax Credit Score Basics

Credit by Equifax

What is an Equifax Credit Score?

For Canadians, the Equifax credit score is a three-digit number between 300 and 900. Lenders use it to decide if you qualify for a loan or a credit card. In our experience, most car buyers have heard of Equifax, but they might not realize it’s one of the two main credit bureaus in Canada.

We see people with all kinds of backgrounds - some new to Canada, some rebuilding after rough patches. Whether it’s someone seeking bad credit loans or looking to build a better borrowing history, the Equifax score is the first thing lenders check.

Definition and Role in Canada’s Financial System

The role of an Equifax credit score is simple. It’s a snapshot of your reliability as a borrower. Banks, dealerships, and car loan companies (ourselves included) rely on it to assess risk. Lower/bad credit scores mean higher risk, so lenders might ask for a bigger down payment, charge higher interest, or even say no. A higher score means better terms - and more “yes” answers.

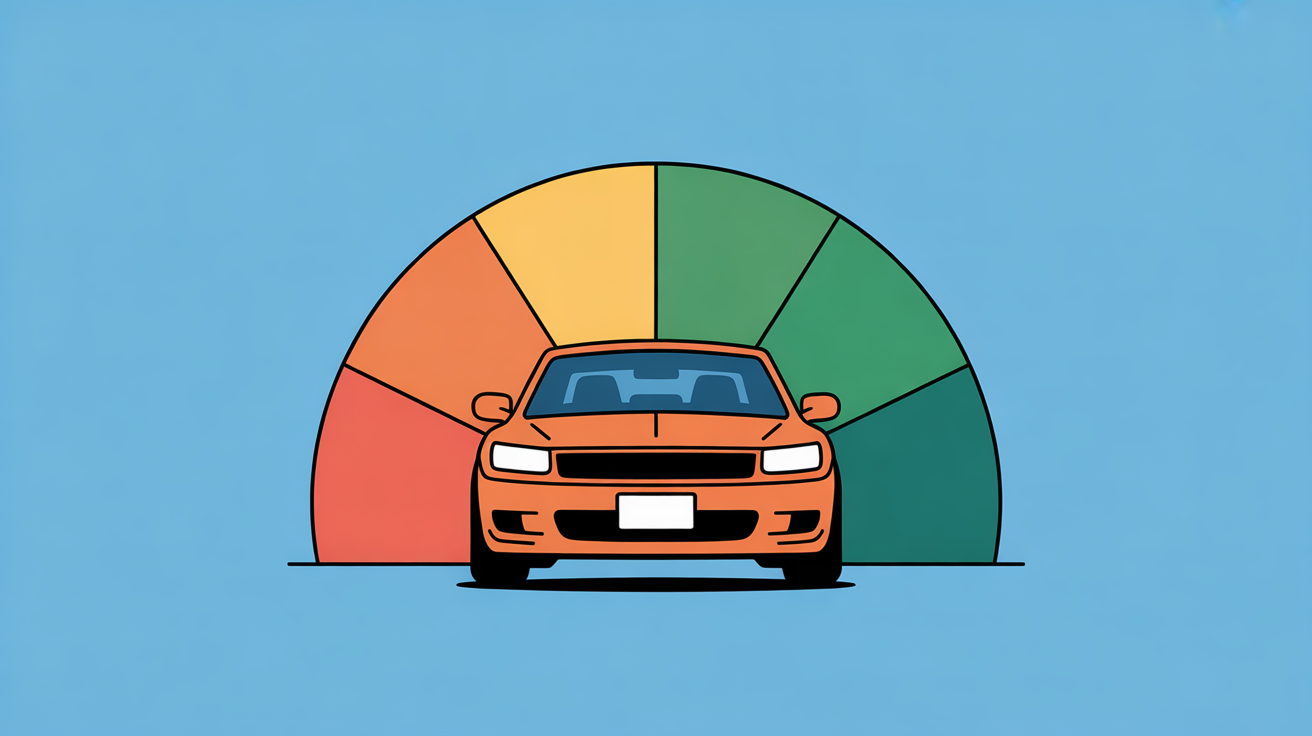

Credit Score Range Explained (300-900)

- 300-559: Poor - very limited access to credit, almost always higher rates.

- 560-659: Fair - some credit options, but still tough to get good rates.

- 660-724: Good - most lenders will consider you, and rates are reasonable.

- 725-759: Very Good - solid approval odds, and you might get preferred rates.

- 760-900: Excellent - best rates and widest options, including zero down at times.

People ask us all the time: What’s a good credit score? In Canada, 660 or above opens most doors.

How Equifax Calculates Your Credit Score

Key Data Sources and FICO Model Integration

The Equifax score isn’t magic. It’s built from the credit report - your history of borrowing and paying back. Equifax uses the FICO model (Fair Isaac Corporation), blending their algorithm with Canadian data. We’ve seen first-hand how even a single missed payment or a maxed-out card can drop a score by 40 to 60 points overnight. The timing of a credit score update explains these sudden shifts. The models are strict, but they aren’t unfair.

Major Factors Considered: Payment History, Debt, Credit Age

Three things matter most:

- Payment History: Have you paid bills on time? This is about 35% of your score.

- Outstanding Debt/Credit Utilization: How much do you owe compared to your limits? That’s another 30%.

- Credit Age: Older accounts help. Lenders like stable, long histories.

There are minor factors too. Recent credit applications and the mix of credit types play a smaller role. [2]

Credit Score Ratings and Their Meanings

Poor, Fair, Good, Very Good, Excellent Explained

Some of our clients come in thinking “fair” means “okay.” It doesn’t. “Fair” is a polite way of saying lenders still see you as risky. “Good” is where doors start opening. “Very good” and “excellent” bring the best rates, the most flexible payment options, and those elusive zero down car loans.

Impact of Each Rating on Loan Eligibility and Interest Rates

- Poor: Harder to get approved, higher down payments, high interest.

- Fair: Possible approvals, but usually higher rates.

- Good: Most options available, decent rates.

- Very Good/Excellent: Top-tier rates, best selection of vehicles, easiest approvals - even for newer cars or trucks.

How to Access Your Equifax Credit Score

Free Online Access via MyEquifax

Knowing how to check your credit score in Canada is easy. You can get your Equifax credit report and score free every month through MyEquifax online. We encourage every applicant to do this before applying.

Alternative Methods: Mail, Phone, In-Person Requests

Not everyone loves online forms. Equifax lets you request your report by mail, phone, or in person at some locations. We’ve even helped a few clients make the call right in our office.

Subscription Options and Benefits

For those who want daily updates, Equifax offers a subscription for around $25 a month after a free trial. This isn’t necessary for most, but it can help if you’re in rebuilding mode or planning a big purchase.

Key Components Influencing Equifax Credit Scores

Payment History and Its Impact

Importance of On-Time Payments

No single habit matters more than paying your bills on time. We’ve seen people with modest incomes and no late payments outscore folks making double just because of consistency. Even one late payment can sting.

Consequences of Delinquencies

Missing a payment? It stays on your report for up to six years. Multiple missed payments can tank your score and make car loans expensive or out of reach for a while.

Credit Utilization and Outstanding Debt

Ideal Usage Ratios for Optimal Scores

Keep balances under 30% of your credit limit. We’ve watched clients boost their score by 20 points in a month by paying down a bit of credit card debt.

Effects of High Balances

Maxed-out cards signal risk. Lenders worry you’re stretched, so scores drop. If you owe $4,000 on a $5,000 limit, that’s 80%, and it drags your score down.

Credit Age and Credit Mix

Role of Length of Credit History

Older accounts show lenders stability. We suggest not closing your oldest card, even if you rarely use it.

Benefits of Diverse Credit Types

A mix of credit cards, loans, and lines of credit looks better than just one type. We’ve seen folks with two credit cards and a small installment loan get better rates than those with one giant line of credit.

Impact of New Credit and Credit Inquiries

How Frequently Applying for Credit Affects Scores

Multiple loan or credit applications in a short span can cost you points. We tell people to limit “hard” inquiries. One or two is fine, but five or six in a few months? Lenders take note.

Managing Credit Checks to Avoid Score Drops

Plan your applications. If you’re shopping for a car loan, do it in a tight window - Equifax recognizes rate-shopping and usually treats it as one inquiry.

Strategies to Improve and Maintain Your Equifax Credit Score

Practical Tips for Credit Score Improvement

- Set reminders for every bill - missing one payment hurts.

- Tackle credit card debt first, especially those above 30% utilization.

- Ask for higher credit limits (without a hard inquiry) to lower utilization.

- Keep old accounts open.

- Limit new credit applications.

We’ve watched clients go from “fair” to “good” in six months just by following these steps.

Credit Score Monitoring and Management Tools

Using Credit Score Simulators and Trackers

Online tools let you see how actions - like paying off a card or opening a new loan - might affect your score. Some find this motivating.

Benefits of Regular Credit Report Reviews

Check your credit report at least once a year. We’ve spotted errors for clients - a wrong address, a paid-off loan still showing as open - that dropped their score. Fixing them usually brings a quick bump.

Addressing Credit Report Errors and Disputes

Identifying Common Errors in Credit Reports

Watch for:

- Incorrect late payments

- Accounts that aren’t yours

- Wrong balances or limits

Steps to Correct Inaccuracies with Equifax

Gather your documents, then file a dispute online with Equifax. They usually respond within 30 days. If you get stuck, we’ve walked clients through the process before.

Long-Term Credit Score Planning

- Set a realistic goal (like reaching “good” or “very good” before applying for a new loan).

- Stick to healthy habits: on-time payments, low balances, regular score checks.

- Don’t panic over small drops - scores fluctuate.

Equifax Credit Score in Context

Comparison with TransUnion and Other Credit Bureaus

Equifax and TransUnion use similar models, but your score can differ by 20 points or more. We’ve seen clients surprised by this when lenders check both. It’s smart to check both scores, especially before a major purchase.

Differences in Scoring Models and Data Collection

Equifax might have some accounts or payment histories that TransUnion doesn’t - and vice versa. Both use the FICO model, but minor differences in data can change your score.

When to Check Multiple Credit Reports

If you’re planning a car loan or mortgage, we suggest checking both bureaus at least once. It’s rare, but sometimes one report has an error that the other doesn’t.

Common Credit Score Myths and Misconceptions

- Checking your own score hurts your credit. (False. Only “hard” inquiries for new credit do.)

- Paying off debt instantly raises your score by 100 points. (Unlikely. Scores take time to adjust.)

- You need a credit card to build credit. (Not true, but having one helps.)

Understanding the Benefits and Risks of Credit Scores

A high score brings lower loan rates, easier approvals, and sometimes better insurance rates. On the flip side, a low score limits your options and can make life expensive. We see this play out every week.

Potential Challenges and How to Overcome Them

- Thin credit file? Open a secured card or small loan.

- Past mistakes? Focus on on-time payments and low balances going forward.

Emerging Trends and Future of Credit Scoring in Canada

Credit scores are evolving. Some lenders now consider rent or utility payments. Algorithms update regularly. We keep an eye on these changes because they affect who gets approved, and at what rates.

FAQ

How does the length of my credit history impact my credit score in Canada?

The length of your credit history refers to how long you have been using credit. A longer credit history can show lenders that you have experience managing credit responsibly. Even if you have a good payment record, a short credit history might limit your score because there is less information to assess your credit habits over time.

Why can a small balance on a credit card sometimes lower my credit score?

Having a small balance on a credit card that you don’t pay off in full each month can affect your credit score. This is because the amount you owe compared to your credit limit, known as credit utilisation, is a key factor. Even a small balance may increase your utilisation percentage, which can lower your score if it goes beyond a certain level.

Can inquiries made by landlords or utilities affect my credit score?

When landlords or utility companies check your credit before offering you services, they might create what is called a “hard inquiry.” These hard inquiries can sometimes reduce your credit score slightly. However, not all checks affect your score, and the impact depends on the type and number of inquiries made over a short period.

How do different types of credit accounts influence my credit score?

Having a mix of credit types, such as loans, credit cards, and lines of credit, can impact your credit score. This is because it shows lenders you can handle different kinds of debt responsibly. However, opening many new accounts at once or mismanaging any type of credit can harm your score rather than help it.

What role does the timing of my payments play in determining my credit score?

The timing of your payments is important because late or missed payments can stay on your credit report for several years. Even if you pay eventually, being late by even a few days can negatively affect your score. Consistently paying on or before the due date helps maintain or improve your credit standing over time.

Practical Advice and Next Steps

We’ve seen hundreds of clients improve their Equifax credit scores by sticking to the basics - pay on time, keep balances low, check your report, and don’t panic over small drops. If you’re thinking about a car loan, knowing your score puts you in control.

Curious about your options, or ready to apply? You can start your application with us here. It only takes a few minutes, and you’ll see how your score shapes your choices - without any obligation.

References

- https://www.equifax.com/personal/education/credit/score/articles/-/learn/what-is-a-credit-score/

- https://www.canada.ca/en/financial-consumer-agency/services/credit-reports-score/credit-report-score-basics.html

Related Articles

Copyright © 2026 Cars with Chloe. All rights reserved.

Cars with Chloe® and the Cars with Chloe Logo are registered trademarks.

Other trademarks are the property of their respective owners.